IMT

Stamp Duty may also be levied on such transfers. The acquisition of more than 75% of the share capital of a limited liability company (as well as a closed privately subscribed real estate investment fund) that owns real estate located in Portuguese territory also determines the incidence of IMT.

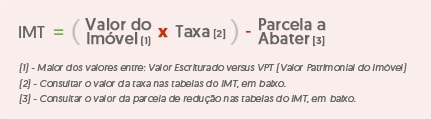

How is the IMT calculated?

The IMT is levied on the higher of two values: the one described in the Sales Contract or the VPT ( Tax Asset Value ) of the property. A fee is applied to this amount (define in the tables below) and any reduction portion is deducted:

If you wish, you can use this IMT calculation simulator to determine the amount to be paid:

(already includes the tables published in the 2018 State Budget)

This calculation tool has purely informative purposes and is not intended to dispense with professional specialized services.

IMT tables for the year 2018

The rates related to this tax, contemplated in the State Budget for 2018, are stipulated as follows:

| Description | Rate |

|---|---|

| rustic buildings | 5% |

| Other urban buildings and other expensive acquisitions | 6.5% |

|

Acquirer residing or headquartered in a country, territory or region subject to a more favorable tax regime (offshore) |

10% |

For properties located on the mainland and for own and permanent housing, the rates are:

| Amount on which the IMT is levied | Marginal Rate to be applied | installment to be slaughtered |

|---|---|---|

| Up to 92.€407 | 5% | €0 |

|

From €92,407 to €126,403 |

two% | €1,848.14 |

| From €126,403 to €172,348 | 5% | €5,640.23 |

|

From €172,348 to €287,213 |

7% | €9,087.19 |

| From €287,213 to €574,323 | 8% | € 11,959.32 |

|

More than €574,323 |

One-off fee of 6% | |

In the case of properties located in the autonomous regions and which are for own and permanent housing, the rates are:

| Amount on which the IMT is levied | Marginal Rate to be applied | installment to be slaughtered |

|---|---|---|

| Up to 115.€509 | 5% | €0 |

|

From €115,509 to €158,004 |

two% | €2,310.18 |

| From €158,004 to €215,435 | 5% | €7,050.29 |

|

From €215,435 to €359,016 |

7% | €11,358.99 |

| From €359,016 to €717,904 | 8% | €14,949.15 |

|

Higher than 717.€904 |

One-off fee of 6% | |

exemptions

- Some facts benefit from exemption, namely those mentioned below, and the exemption may be subject to the verification of certain requirements:

- Acquisition of buildings for resale by real estate companies;

- Acquisition of urban buildings intended for urban rehabilitation;

- Acquisition of buildings or autonomous fractions for the installation of qualified enterprises of tourist utility;

- Acquisition of properties by Real Estate Investment Funds for Housing Lease;

- Restructuring operations or cooperation agreements;

- Acquisition ofbuildings classified as of national/public/municipal interest;

- Exemption or reduction of IMT in relation to the acquisition of buildings that constitute relevant investments, within the scope of the Tax Regime for Investment Support (RFAI).

Important Note: The information in this glossary is for informational purposes only. For proper advice on legal or tax matters, consultation with a duly authorized lawyer, notary, solicitor, or accountant is essential.

Your next step in the real estate market

Whether you want to sell your property for the maximum value or find the ideal home, count on my experience as a Top Producer consultant at KW Portugal. Talk to me without obligation. Start today with a simple contact.

Contact Me Today

Related articles

Follow me

on Social Media