The Portuguese real estate market has faced significant challenges due to variations in interest rates. In June, interest represented more than half of the mortgage loan payment, directly affecting owners and potential buyers.

The Situation in Portugal

In June, the interest rate implicit in home loan contracts reached 3.649%, the highest value since April 2009. This increase resulted in an increase in the average mortgage installment to 361 euros, an increase of 38.3% compared to June of the previous year.

According to the Bank of Portugal, there are more than one million home loan contracts , which means that between 2 and 3 million Portuguese people are affected by the impact of rising interest rates. The average duration of home loan contracts in Portugal has remained stable, with the majority of Portuguese opting for terms between 20 and 30 years.

On the other hand, 42% of bank credit is allocated to the 20% of Portuguese who have the highest salaries . In short, if we divide Portuguese society into five blocks – from families with the lowest income to the most affluent families – only 6% of credit is in the block with the lowest salaries. And practically two thirds of the credit is in the two blocks that earn the most. Perhaps this is one of the reasons why despite the “default risks” in credit, the number of seizures, despite the brutal increase in interest rates, is still relatively low.

European Central Bank Decisions

The European Central Bank (ECB) has been active in its approach to interest rates. Recently, the ECB decided to increase its main interest rates by another 0.25 percentage points. This was the ninth consecutive rise in a year, in an attempt to control galloping inflation in the euro zone.

Christine Lagarde, president of the ECB, indicated that there may be a pause in interest rate hikes or that rates may have already reached their peak. However, the only certainty is that there will be no reduction in interest rates in September.

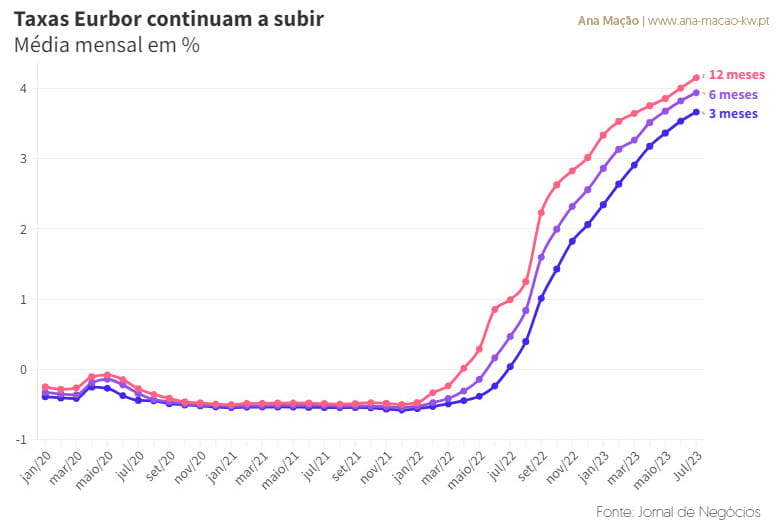

Euribor rates, which serve as an index for most home loan contracts in Portugal, have suffered dizzying increases. In March of the previous year, the 12-month Euribor was rising, anticipating the ECB's interest rate hike, but it still showed negative values. However, the July average shows that the 12-month Euribor exceeded 4%, with the 6-month Euribor close to 4% and the three-month rate above 3.6%.

Impact of Euribor Rates

This scenario has direct implications for mortgage loan installments. For example, for a loan of 150 thousand euros over 30 years, indexed to the 12-month Euribor and with a spread of 1%, the increase in the installment can exceed 280 euros. If the contract is indexed to Euribor 6 months, the increase in installments may exceed 95 euros, representing an annual increase of more than 284 euros.

Interest Rate Forecasts

In the coming months, interest rates in Portugal and the euro zone are expected to continue their upward trend. This forecast is based on several factors, including the post-pandemic economic recovery, rising inflation and the monetary policies adopted by the European Central Bank (ECB), as well as the homonymous American Federal Reserve.

The ECB has signaled the possibility of increasing interest rates to combat inflation and stabilize the economy. However, it is important to note that any decision taken by the ECB will have a direct impact on interest rates in Portugal, given its integration into the euro zone.

Conclusion

Interest rates play a crucial role in the real estate market. With recent increases, it is essential that owners and potential buyers are informed and prepared for possible fluctuations. ECB decisions and variations in Euribor rates have direct implications for monthly installments, and it is crucial to be aware of these changes when making decisions related to the real estate market.

Consider carefully what type of credit you plan to take out, whether variable and indexed to the Euribor Rate or whether you choose a fixed rate installment. The Government is considering legislating to facilitate the temporary change of this regime, for those who already have contracts in force, during a transitional period of 2 years. Be aware.