After the publication of the OE for 2017, changes to the fiscal framework for this year are already known, with regard to the real estate sector. Not everything that has been said over the past few months has taken the form of a law and some surprises have emerged, in a budget that had real estate at the center of the discussion, not always for the best reasons.

So, here are the main tax changes for the current budget:

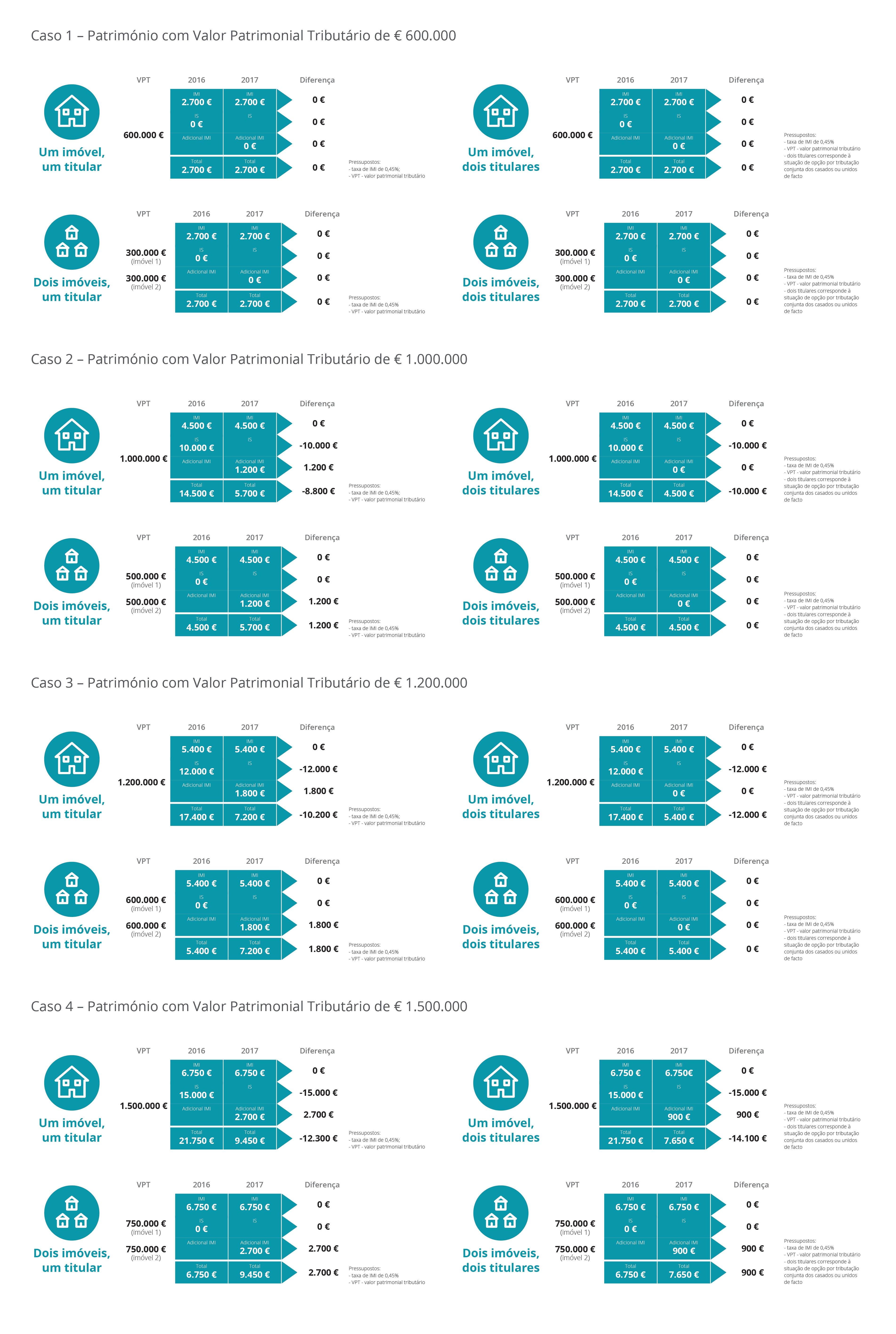

Additional to the Municipal Property Tax (AIMI)

The big news, also known as "Mortágua Tax", due to the way it was announced, this new tax is not really a new tax as it replaces, according to new models, the previous stamp duty additional to IMI, in force since 2014 ( 1% for VPT greater than 1 million euros). Unlike IMI, it is not a municipal tax, as it reverts directly to the state coffers.

The new tax applies to all taxpayers, both natural and collective , who hold a real estate heritage ( urban buildings intended for housing, or land for construction ), whose global value exceeds € 600,000 . The rates to be applied depend on:

- In the case of individual taxpayers and undivided inheritances, the rate will be 0.7% on the part that exceeds € 600,000. If this value exceeds € 1,000,000, then the rate to be applied will be 1% of the amount that exceeds this level. Married or de facto unpaid taxpayers may opt for joint taxation, in which case the VPT's of the properties will be added together, and may deduct up to € 1.2 million.

- If it is a collective taxpayer, the single rate to be applied will be 0.4% of the global asset value, with no deduction of € 600,000 in the tax, as observed by individual taxpayers. If the properties are intended for the personal use of the capital holders, members of the governing bodies or any bodies of administration, management or inspection, the rate to be applied is 0.7%. Even in this case, if the VPT is greater than € 1,000,000, a marginal rate of 1% will be applied.Companies may also exceptionally deduct € 600 thousand, if they have properties whose VPT is directly allocated to its operation.

Urban buildings classified as “commercial, industrial or for services” and “other” are exempt from paying AIMI.

The option of deducting AIMI from the IRS is now limited to the fraction of the collection corresponding to the income generated by properties subject to AIMI, within the scope of rental or accommodation activities.

Collective entities may choose to deduct the amount paid as AIMI under IRC, deducting it either from taxable profit or from collection (if the properties are to be leased). You can see a simulation for several scenarios here.

In the case of undivided inheritance, there is the option of presenting a declaration by the head of the couple, identifying the heirs and their respective quotas, with the share of each heir being added to the sum of the tax assets of the buildings of which it is. holder individually.

Compared to the previous stamp duty on luxury properties, which is thus extinguished, the big change is that now, it is not the individual properties that are taxed, but the taxpayer's global assets. On the other hand, the tax increase is levied on the average value assets, and in some cases the owners of higher value properties may suffer a tax relief.

The consultancy Deloitte presented a set of simulations that help to understand the impact of this tax depending on the profile of the owner.

Local accommodation

Taxpayers under the simplified regime, who declare income obtained through the exploitation of the local accommodation activity (namely through the short-term rental of houses or apartments, via Airbnb or others), will suffer an increase, with the coefficient to be applied for determination of taxable income goes from 0.15 to 0.35, in 2017.

That is, for every € 100 of income, only € 35 is taxed, that is, if they opt for the declaration in category B as corporate income, alternatively, they can opt for taxation as property income (category F), whose rate is 28% .

IMI

The exemption from IMI, for those who can benefit from it and who until now had to submit an application to the Tax and Customs Authority (AT), started to be automatically assigned. This exemption is valid for 3 years for urban housing buildings constructed, expanded, improved or acquired against payment, intended for the taxpayer's or his household's own permanent residence.

This exemption is limited to urban housing buildings with a VPT of less than € 125,000, intended for the taxpayer or his household's own permanent residence, whose taxable income, for IRS purposes, in the previous year is not greater than € 153,300.

Non-resident taxpayers are excluded from the IMI exemption, even if they have low income.

The municipalities saw the maximum ceiling for reducing the IMI rate from 15% to 25% for urban buildings with high energy efficiency. This discount is optional and can be applied after deliberation by the municipal assembly.

Dams, multipurpose pavilions, swimming pools, golf courses, windmills and water mills, campsites, car wash facilities, stadiums, electro-producer centers, telecommunications towers, fuel filling stations are now taxed with IMI. such is the formula already applied to land taxation: the value of the land plus construction costs.

It is foreseen in the current budget, that within 120 days after its publication, the assembly of the republic will legislate in order to redefine the criteria for the evaluation of rustic buildings and, thus, create the necessary conditions for the evaluation. It should be remembered that the tax charged for this type of property is generally low and proportional to its equally low equity value.

{kind=link}